How bonds shaped wars, empires, and the economy

The Transformative Power of Bonds

Hi there,

Investing in the stock markets allows us to participate in the broader economy, it is one of the pillars of modern finance.

However, equity isn't the only way companies and governments raise money. In fact, there is a much older method- debt.

Debt markets have been around since 2400 BC when the first bonds were created in Nippur, in Mesopotamia, now present-day Iraq. The borrower would make payments in grain to the lender.

In modern times, the bond market is a crucial part of the larger debt market. And though invisible to most of us, the bond markets play an important part in our lives.

Don’t believe me? Read on and hopefully by the end I'll have convinced you of their importance through a collection of anecdotes.

So, what is a modern-day bond?

As per The Economist,

IOUs issued by a borrower which normally promise repayment of the money on a set date (the maturity) with regular interest payments during the life of the bond. The more risky the issue, the higher the interest rate (or yield) on the bond. Governments issue bonds to cover the gap between the amount they receive in taxes and the amount they spend. Companies issue bonds to finance investment programmes

Furthermore, there are a few key differences between a bond and its sibling; a loan

A bond is designed to be bought and sold. This aspect has been key to their growth as an instrument.

The market is made up of a wide range of participants - such as banks, institutions, pension funds, and countries looking to borrow and invest. Today, bond trading happens by phone, electronic messages and algorithms across the world’s financial centres. Bonds are designed to be traded, while loans are typically not.

A loan's cost usually fluctuates as it is pegged to a central bank's interest rate or some other agreed benchmark such as LIBOR, while most bonds pay a fixed rate.

To understand the importance of the bond market today, let's travel to medieval Italy.

The perils of lending in medieval Italy

Prior to the concept of bonds, whenever a regime needed money, usually to go to war - they raised it via taking out a loan or raising taxes from citizens. Both of these approaches came with problems.

Raising taxes fueled discontent but why was taking a loan a problem?

Consider the case of Florentine bankers,

In the 13th century, Florence was the banking center of Europe, specializing in lending to monarchs to finance wars. Edward III of England borrowed vast sums at sky-high interest rates from Florentine bankers to equip his army against France in the Hundred Years' War.

The bankers extended these loans against grants of wool, money, and assignment of customs and taxes. Eventually feeling the pinch, the English crown cancelled large parts of the debt and forced the bankers to forgo their interest claims. Unable to sustain losses, eventually a prominent banking family, the Peruzzi family, filed for bankruptcy.

The problem of being tied to one big borrower and loaning them more and more to protect the money already given was problematic.

The bankers lacked the tools we have today to distribute the risk if the borrower does not pay. The financial guardrails which allow lenders to share the risk of default with others did not exist.

The fall of bankers, added to the economic decline of Florence and the setback affected all parts of society, the rich and the poor.

The dawn of tradable loans in Venice

Prior to the crisis unfolding in Florence (above), tradable loans had begun to emerge in Venice.

In 1171, the Venetian ruler Doge Vitale II Michiel needed to launch a rescue mission to retrieve hostages captured by the Byzantines. To fund this operation, he forced citizens to lend the city money so he could build a fleet. In return citizens would be paid 5% interest annually until the principal was repaid.

Unfortunately, things did not go his way. A plague destroyed the Venetian fleet and the Doge returned humiliated and broke. Unable to repay the angry citizens, Venice was forced to convert their obligations into an instrument that would pay 5% interest in perpetuity.

Slowly, over time, the arrangement worked well for both the government and citizens. The citizens were happy with the steady 5% income, while the city could raise money as needed.

The loans, called prestiti, became so popular they were bought and sold in the city's markets. This tradability differentiated the Venetian loans from earlier debt instruments.

Such was their importance that,

trading the prestiti became popular by the 13th century. Venetian nobles traded them for charity and to add to their daughters’ dowries. Market rates were publicly available, and purchasers would have the same rights as the original bondholders. Thus by the late 1200s, … , Venice had its own secondary market for bonds.

Source: Bonds Part VI: An Overview of Medieval Venetian Finance | Financial Modeling History (wordpress.com)

Risk became transferable. When the risk became too much to handle or weighed too heavily on one's finances, it could be traded to others for self-protection.

One could speculate that if the Florentine bankers had learned from the Venetians and issued tradable loans, they could have transferred their risky debts to other financiers with healthier balance sheets and avoided bankruptcy.

How bonds changed the world

Since then, bonds have acted as a vehicle for long-term borrowing, allowing borrowers to invest the money raised into major projects.

For example,

Britain’s victory over France during the Napoleonic Wars was partly due to England’s ability to raise loans through its financial system. Its track record as a reliable debtor meant people were willing to invest in its debt at relatively low interest rates. France, on the other hand, had ruined its reputation in recent decades and had to rely on short-term, high-interest loans. Thus, even though France was the stronger military power, Britain prevailed.

The U.S. nearly doubled in size after the Louisiana Purchase, which stretched from the Gulf of Mexico to Canada, and from the Mississippi River to the Rocky Mountains.

Although the purchase was a bargain at $15 million, it exceeded what the young U.S. treasury could afford at the time.

Banks in England and Amsterdam facilitated the deal by purchasing the land from France and forwarding the payment. The banks simultaneously purchased U.S. government bonds, which would repay the principal over 15 years at 6% interest, using the land as collateral against potential U.S. default.

Each of these momentous events was made possible by the availability of bonds, which financed initiatives at scales unachievable through taxation or individual wealth alone. Throughout history, access to bond markets has enabled governments and institutions to fund ambitious projects and expand their spheres of influence.

Bonds in modern times

In modern times, the popularity and global reach of bonds continues to grow.

Tesla has often tapped the bond market to raise money to ramp up production. In 2023, it plans to raise $1 billion from the bond market, while backing it up with collateral from leases taken on by select customers of Tesla’s new EV.

The Indore Municipal Corporation raised Rs. 244 crores to fund a solar power project. This marked the first time a local government body in India raised money directly from retail investors. They offer a coupon rate of 8.25% per annum, payable half-yearly with tenure of 3-9 years.

From companies seeking to expand, to municipalities funding local infrastructure, bonds remain an essential source of financing for organizations of all sizes pursuing long-term growth and development. The global bond market continues to evolve as a vital pillar supporting economic progress worldwide.

So how does the bond market impact you?

The key is interest rates, which indicate the cost of borrowing and are benchmarked globally against U.S. Treasury yields.

We talk about the U.S. because it dominates the global bond market. In 2022, the global bond market totaled $133 trillion out of which the U.S. market was valued at $51 trillion, 38% of the market.

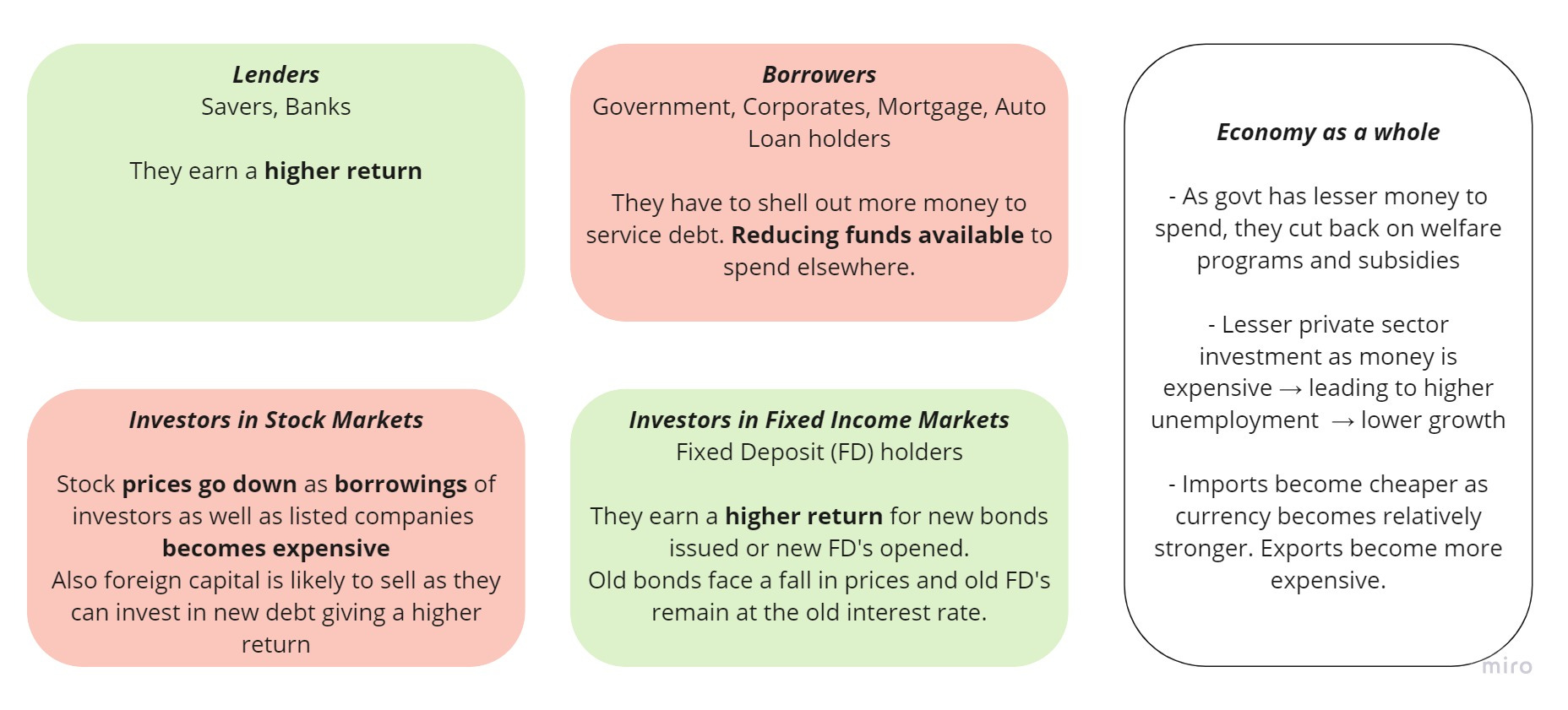

When interest rates rise (money is more expensive to borrow), bond prices fall as a bond paying a fixed amount is worth less. This is the situation we find ourselves in today.

Here’s how to think about the impact of higher interest rates on the economy

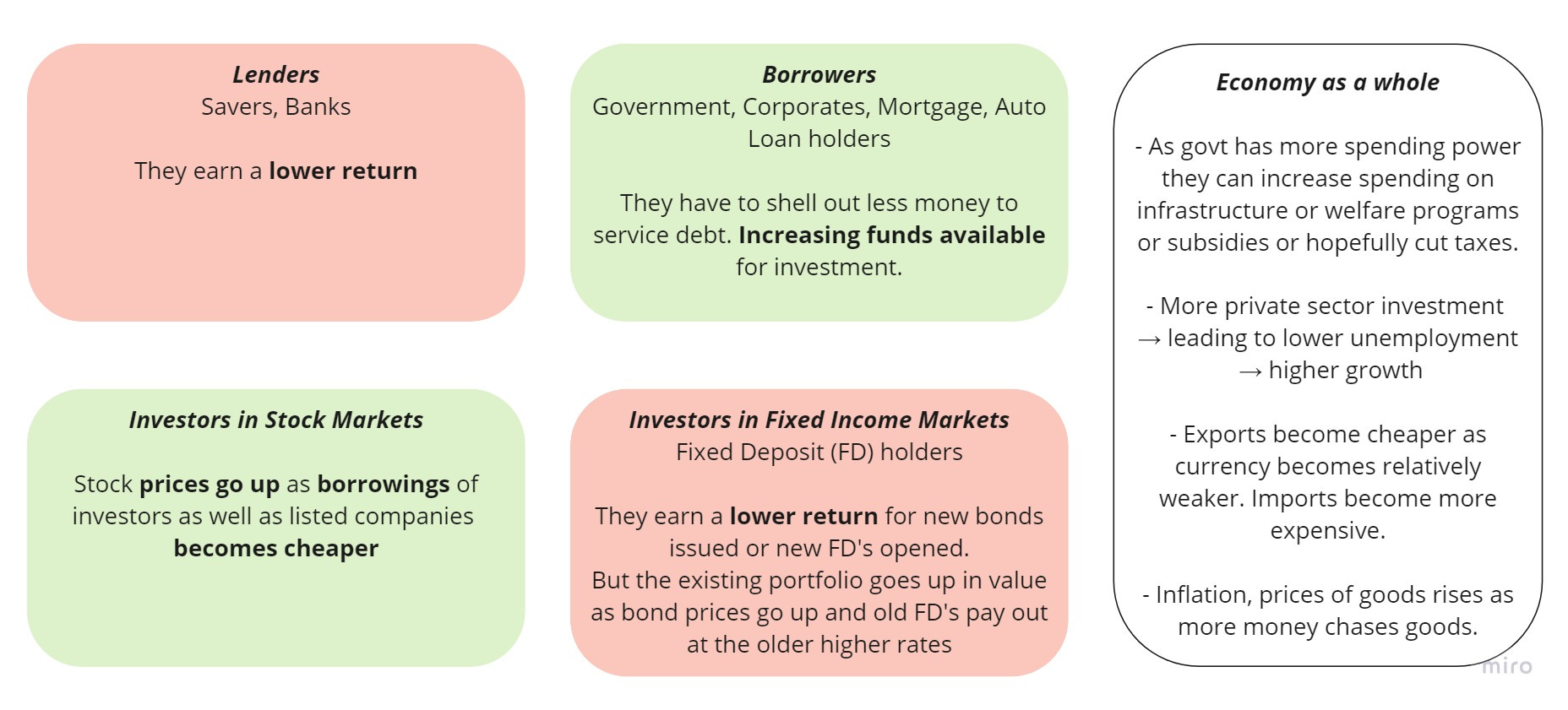

When interest rates go down (money is cheaper), bond prices go up as investors value the higher fixed coupon more. This is what happened post mid- 2020 when U.S. started pumping money into the system till mid-2022.

Here’s how to think about the impact of lower interest rates on the economy

Changes in interest rates affect the affordability of mortgages, car loans, corporate investment and government spending. Bond markets may seem abstract but they influence the real economy profoundly. To understand more read this brilliant article by Vivek Kaul- What ‘they’ did not tell you about home loan interest rates

Wrapping up,

I hope these stories gave you a better appreciation for the transformative role that bonds have had throughout history. From wars to territorial expansions and now the march towards electric vehicles, bonds have been at the heart of enabling significant events to unfold.

Bonds have made risk tradable and facilitated the flow of money, silently powering economies worldwide.

While the bond market may not always be in the limelight, its influence is undeniable. It's a testament to human creativity in solving financial challenges and shaping progress.

If you have any stories or insights about bonds, I would love to hear them in the comments.

Filtered Kapi #48